Medicaid Spenddown Explained: How It Works & Examples | MedXCode

John Doe

Retirement should be a time of peace and comfort not financial anxiety.

However, many older adults living on limited pensions or Social Security face overwhelming healthcare costs that strain their budgets.

This is where Medicaid steps in.

Medicaid is a government-funded health insurance program designed to help individuals who cannot afford medical care. For millions of seniors, it offers financial protection and access to necessary healthcare services without risking financial collapse. Running a small medical practice means balancing patient care often face financial strain when handling high Medicaid patient volumes.

Is Medicaid Spenddown Helpful for Americans?

For individuals struggling with medical expenses, Medicaid can be a vital safety net. It provides healthcare coverage for people with limited income and financial resources.

Still, many Americans fall into a difficult gap earning slightly too much to qualify for Medicaid, yet not enough to comfortably pay for insurance premiums and medical bills.

To solve this problem, certain states offer Medicaid Spenddown programs. These programs allow individuals to subtract approved medical expenses from their income to meet Medicaid eligibility requirements. By paying out-of-pocket for prescriptions, doctor visits, and hospital services, individuals can reduce their effective income to qualify for Medicaid benefits.

What Does “Medicaid Spenddown” Mean?

Medicaid eligibility is determined by income and asset limits set by each state. When an individual’s income exceeds these limits, they may still qualify through a process known as Medicaid Spenddown.

This method requires individuals to use part of their income on medical expenses until their income aligns with Medicaid’s required threshold.

Example

If an elderly person earns $1,400 per month and their state’s Medicaid limit is $1,200, they must spend $200 on eligible medical expenses such as insulin, medical supplies, or prescriptions to qualify.

Key Things to Know About Medicaid Spenddown

Many applicants earn more than their state’s Medicaid income limit. To become eligible, they must reduce excess income through medical spending. This process works as follows:

- Individuals can reduce countable income monthly by paying approved medical costs

- Expenses like doctor visits, hospital stays, prescriptions, and treatments qualify

- Keeping accurate records, receipts, and medical bills is essential

- The spenddown process must be repeated if income exceeds limits again

- Once excess income is reduced to the allowed threshold, Medicaid benefits begin

In short, Medicaid Spenddown provides a financial bridge for individuals caught between earning “too much” and still being unable to afford healthcare.

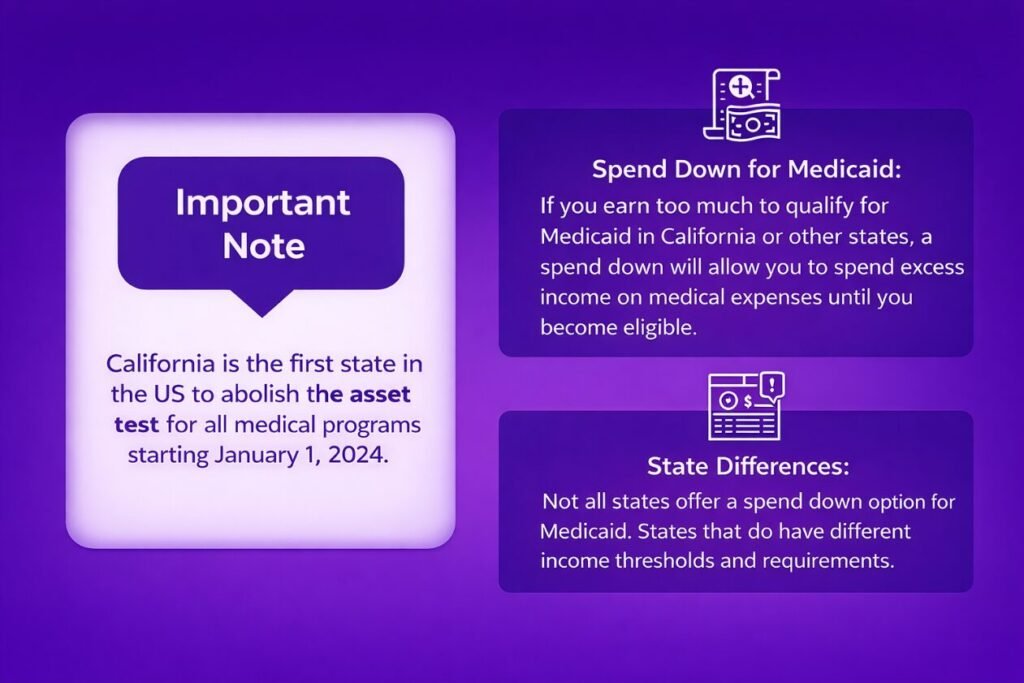

Did You Know?

California has expanded Medicaid access by removing asset limits from several healthcare assistance programs increasing eligibility regardless of income or savings.

Types of Medicaid Spenddown

Depending on a person’s financial situation, Medicaid Spenddown may apply to income, assets, or both.

1) Income Spenddown

This option helps seniors whose monthly earnings exceed Medicaid’s income limit.

They can lower their countable income by paying medical costs such as:

⦁ Physician appointments

⦁ Outstanding medical bills

⦁ Prescription medications

⦁ Health insurance premiums

Example

A Florida senior earns $3,000 per month in 2024. The Medicaid income limit is $2,829, meaning they exceed the limit by $171. If they spend $171 on medical expenses, they qualify.

Some states allow excess income to be placed into a Qualified Income Trust (Miller Trust), which is used to cover medical or long-term care expenses.

Medicaid Asset Limits by U.S. State

| State | Individual Asset Limit | Couple Asset Limit |

|---|---|---|

| Alabama | $2,000 | $3,000 |

| Alaska | $2,000 | $3,000 |

| Arizona | $2,000 | $3,000 |

| California | No limit | No limit |

| New York | $30,182 | $40,821 |

| Texas | $2,000 | $3,000 |

| Florida | $2,000 | $3,000 |

Countable vs. Non-Countable Assets

- Countable Assets These are financial resources that can be used to pay for healthcare, such as savings accounts, investments, or cash holdings.

- Non-Countable Assets These assets are excluded from Medicaid eligibility calculations, including a primary residence or certain personal belongings even if they hold significant value.

- Countable Assets These are financial resources that can be used to pay for healthcare, such as savings accounts, investments, or cash holdings.

- Non-Countable Assets These assets are excluded from Medicaid eligibility calculations, including a primary residence or certain personal belongings even if they hold significant value.

Medicaid Income Limits (Updated May 2024)

Alabama

| Medicaid Type | Single | Married (Both) | Married (One Applies) |

|---|---|---|---|

| Nursing Home Medicaid | $2,829/month | $5,658/month | $2,829/month |

| HCBS Waivers | $2,829/month | $5,658/month | $2,829/month |

| Regular Medicaid | $963/month | $1,435/month | $1,435/month |

What Is the Medicaid Spenddown Period?

The Spenddown Period is the timeframe (typically 1 to 6 months) allowed for individuals to reduce income by paying medical expenses.

Example

A single mother in Connecticut earns $2,000 per month, but the Medicaid limit is $1,600. She must spend $400 on eligible medical costs within the allowed timeframe to qualify.

To remain eligible, individuals must meet spenddown requirements every month.

What Happens If Spenddown Requirements Aren’t Met?

Failing to spend enough income during the allowed timeframe may result in temporary loss of Medicaid coverage, creating financial strain and healthcare gaps.

People can seek guidance from the State Health Insurance Assistance Program (SHIP), which provides counseling and Medicaid eligibility support.

Because Medicaid spenddown rules can be complex, accurate record-keeping and expert advice are strongly recommended.

Medical Expenses That Qualify for Spenddown

Eligible expenses generally include:

- Personal medical bills (doctor visits, prescriptions, hospital stays, medical devices)

- A spouse’s medical expenses

- Healthcare costs for dependent children

- Outstanding unpaid medical bills

- Expenses not covered by Medicare or private insurance

Who Is Eligible for Medicaid Spenddown?

Spenddown programs typically apply to individuals in these groups:

- Children under age 21

- Adults aged 65 and older

- Individuals who are blind or disabled

How to Calculate the Medicaid Spenddown Amount

Formula

(Monthly Income − Medicaid Income Limit) = Spenddown Amount

Example

If a person earns $2,500 per month and their state Medicaid limit is $2,000, they must spend $500 on medical expenses before Medicaid begins covering care.

What Is “Extra Help” for Medicaid Recipients?

Individuals who qualify for Medicaid through Spenddown may also qualify for Medicare Extra Help, a program that reduces prescription drug costs.

Extra Help lowers out-of-pocket expenses for Medicare drug coverage and applies to individuals enrolled in both Medicaid and Medicare.

People approved for Medicaid Spenddown within the last six months automatically qualify for Extra Help for the remainder of the year.

Frequently Asked Questions

1.What is Medicaid Spenddown?

Medicaid Spenddown is a process that allows individuals whose income exceeds Medicaid limits to qualify by spending excess income on approved medical expenses.

2. Who qualifies for Medicaid Spenddown?

Spenddown is typically available for seniors, people with disabilities, blind individuals, and children under 21 who exceed Medicaid income limits.

3. What medical expenses count toward Medicaid Spenddown?

Eligible expenses include doctor visits, prescriptions, hospital bills, unpaid medical bills, insurance premiums, and medical equipment not covered by insurance.

4. What is the difference between income spenddown and asset spenddown?

Income spenddown reduces monthly earnings through medical expenses, while asset spenddown reduces countable financial resources to meet Medicaid eligibility requirements.

5. How long is the Medicaid Spenddown period?

The spenddown period generally ranges from 1 to 6 months, depending on state Medicaid regulations.

6. What happens if I don’t meet spenddown requirements?

Failure to meet spenddown limits may result in temporary Medicaid coverage loss until eligibility is restored.

7. How does MedXCode help with Medicaid Spenddown?

MedXCode provides expert Medicaid billing, eligibility verification, claims processing, and revenue cycle management to ensure accurate coverage qualification and faster reimbursements.